Chile’s Economic Development Path

Stability, Openness, and the Next Growth Model

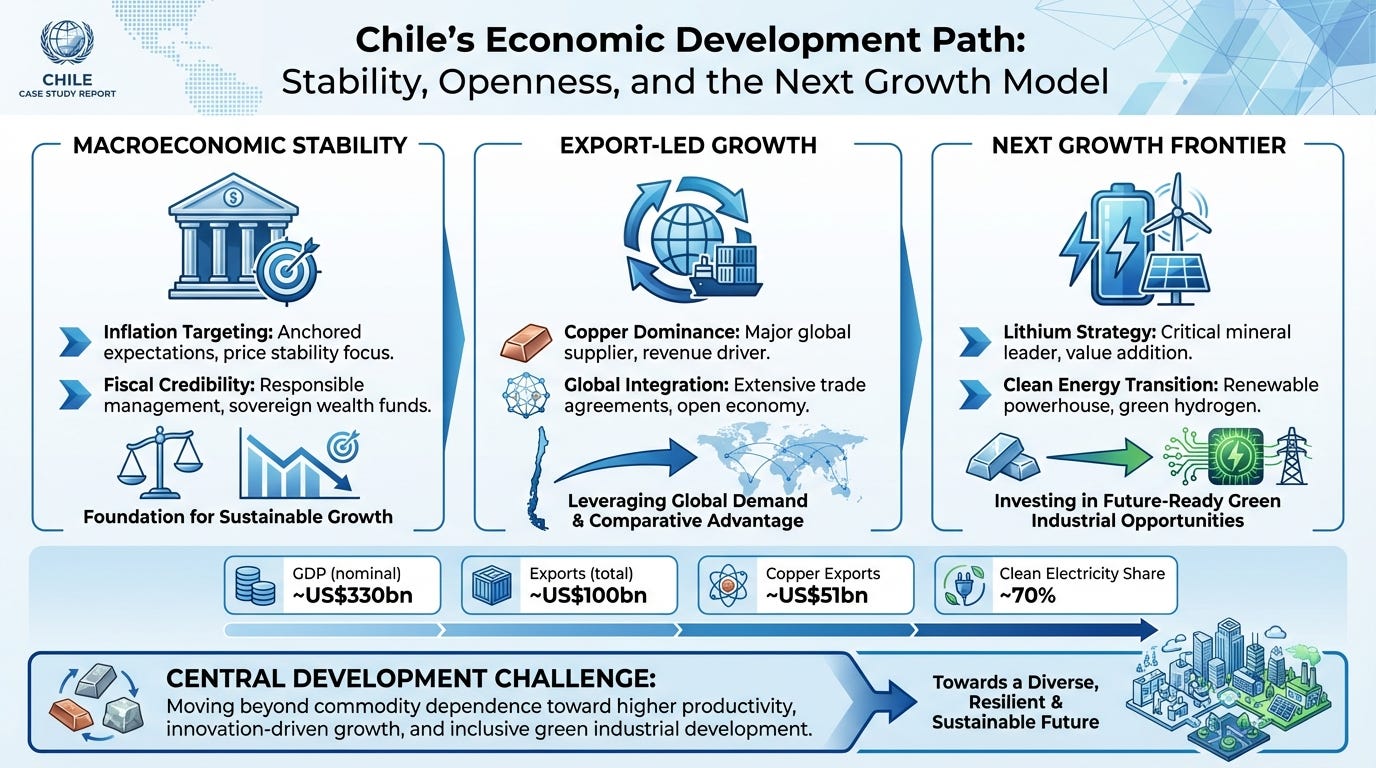

Chile is often treated as Latin America’s reference case for long-run economic development: an economy that combined rules-based macroeconomic management, deep trade integration, and targeted social policy to deliver decades of poverty reduction and rising living standards. Today, Chile is a high-income economy by World Bank classification, with 2024 GDP of roughly US$330bn and GDP per capita around US$16,700.

The current development challenge is less about “getting to middle income” and more about escaping a low-productivity equilibrium while sustaining social legitimacy and navigating a global green transition. Near-term macro conditions improved through 2024–H1 2025—growth recovered, inflation decelerated, and fiscal consolidation resumed—but unemployment and weak job creation highlight structural constraints.

Chile’s next phase of development can be understood through a live policy experiment: using its world-class natural resource base (copper and lithium) and rapidly greening power system to build a more diversified, innovation-orientedeconomy—without repeating the classic pitfalls of commodity dependence (volatility, enclave growth, local conflict, environmental stress).

1) Starting point: where Chile is today

Chile’s economic model rests on three mutually reinforcing pillars:

Macroeconomic credibility anchored in an inflation-targeting regime and a floating exchange rate (explicitly aiming for 3% inflation over a two-year horizon).

Rules-based fiscal management, including a structural balance approach that has guided fiscal policy since 2001, shifting attention from the headline balance to a medium-term, cyclically adjusted position.

Global integration through an unusually dense network of trade agreements—spanning the United States, the European Union, China, CPTPP and multiple regional partners—supporting market access and investment.

Current macro snapshot (2024–mid 2025)

After a subdued 2023, real GDP growth recovered to ~2.6% in 2024, and expanded around 2.8% year-on-year in H1 2025, led by exports and a modest rebound in demand.

Inflation remained above target but moved in the right direction: it was 4.3% y/y in July 2025, and the central bank resumed easing, cutting the policy rate to 4.75%.

On the social side, poverty (measured at US$8.30/day, 2021 PPP) was estimated at ~5.5% in 2024, while income inequality (Gini) stood around 43.1—down from prior years but still elevated by OECD standards.

The labour market, however, signalled the binding constraint. As of June 2025, unemployment was ~8.9%, and informality around 26% (higher for women), reflecting sluggish job creation outside capital-intensive sectors.

2) The trade-and-resources engine: strong, but concentrated

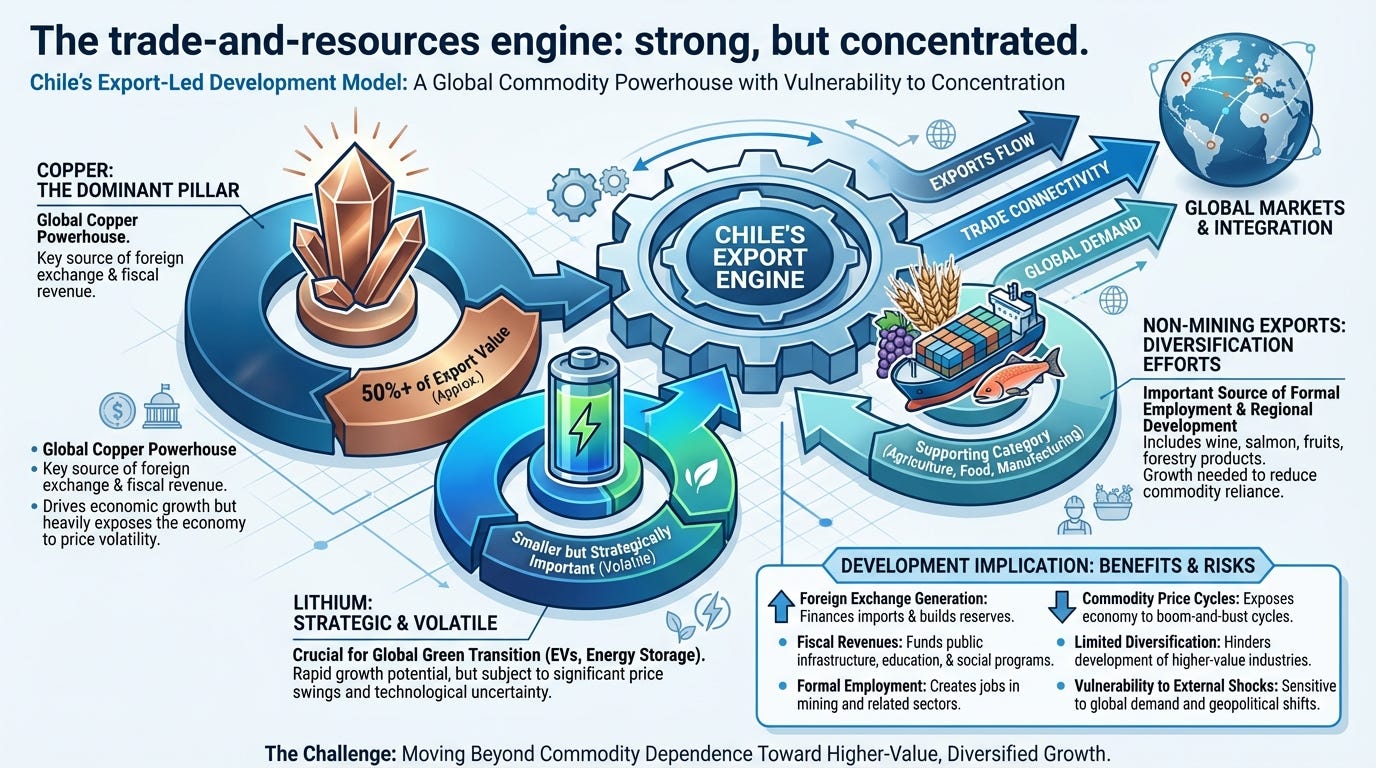

Chile’s export sector remains the backbone of its growth model—and the source of both resilience and vulnerability.

Exports: scale, partners, and composition

In 2024, Chile recorded goods exports of US$100.163bn (a historic level, though slightly down year-on-year), with China and the United States as the two largest destination markets.

Export composition underscores concentration:

Copper exports were US$50.858bn in 2024—roughly half of goods exports by value.

Lithium exports fell sharply to US$2.893bn (reflecting price-cycle dynamics and volatility).

Non-mining exports (food, agriculture, forestry, etc.) were sizeable and growing, including processed foods and fruit exports.

Trade is also meaningful for employment: Chile’s exporters were associated with ~1.17 million formal jobs (about 12%of formal employment), indicating that export performance is not purely an “enclave” tale.

Copper: global leadership, strategic relevance

Chile remains the world’s central copper supplier. In 2024, Chile’s mine production was about 5.3 million tonnes (copper content), and it held the largest copper reserves (about 190 million tonnes).

Copper’s development relevance is twofold:

It provides foreign exchange, tax revenues, and a platform for sophisticated supplier ecosystems (engineering, services, logistics).

It is a critical input for electrification globally—creating an opportunity to link commodity advantage to higher value-added capabilities (processing, services, low-carbon certification, industrial innovation).

State capacity is central here. Chile’s state-owned miner, Codelco, reported total copper production of ~1.442 million tonnes in 2024 (including stakes in major joint assets), and substantial capital expenditure programmes—illustrating how state enterprises remain systemically important.

3) Case study: building “next-generation” growth from lithium + clean power

The development question

How can Chile convert a world-class position in critical minerals into broad-based, sustainable development, rather than a narrow rent economy?

Chile’s policy response has been to pursue a state-steered, public–private strategy in lithium—explicitly linking the sector to economic development goals (value creation, capability building, and sustainability), while using the greening electricity system as a competitiveness lever.

A) Lithium: scale, volatility, and the strategy choice

Chile is one of the world’s leading lithium producers. In 2024, Chile produced roughly 49,000 tonnes of lithium (content), around one-fifth of global mine production, and held reserves of approximately 9.3 million tonnes.

But the 2024 export downturn demonstrates the core policy problem: lithium is a high-volatility development asset.

Chile’s National Lithium Strategy (2023) is designed as a public–private collaboration in which the state provides long-term direction and regulation while private actors contribute capital, technology and market networks.

Key design elements frequently emphasised in official summaries include:

A stronger state role across the value chain, including the planned National Lithium Company and an expanded role for state mining firms (notably Codelco and ENAMI) in project development.

Institutional modernisation and a focus on sustainability—recognising that salt flats are fragile ecosystems and that long-term social licence depends on environmental safeguards and local participation.

Development logic: Chile is effectively attempting to replicate what it historically did well in copper—combining state stewardship and macro credibility with private capability—while correcting what it did less well: moving far enough up the value chain and building domestic innovation intensity.

B) Clean electricity: an enabling platform for competitive, low-carbon industry

A second leg of the strategy is energy. Chile’s government reports that close to 70% of electricity generation now comes from clean sources, reflecting a rapid shift in the power mix.

This matters for development because it creates potential comparative advantage in:

Low-carbon mining and metals (a growing requirement in global supply chains).

Green hydrogen and e-fuels (where abundant renewables can translate into exportable energy-intensive products over time).

Investment attraction for firms looking to decarbonise production footprints.

In practice, the “binding constraints” move from generation to transmission, storage, permitting, water management, and community consent—the unglamorous institutional and infrastructure conditions that determine whether green growth scales.

4) Constraints: why Chile’s model is under pressure

Chile’s near-term macro stabilisation does not remove deeper structural challenges.

The core constraints are:

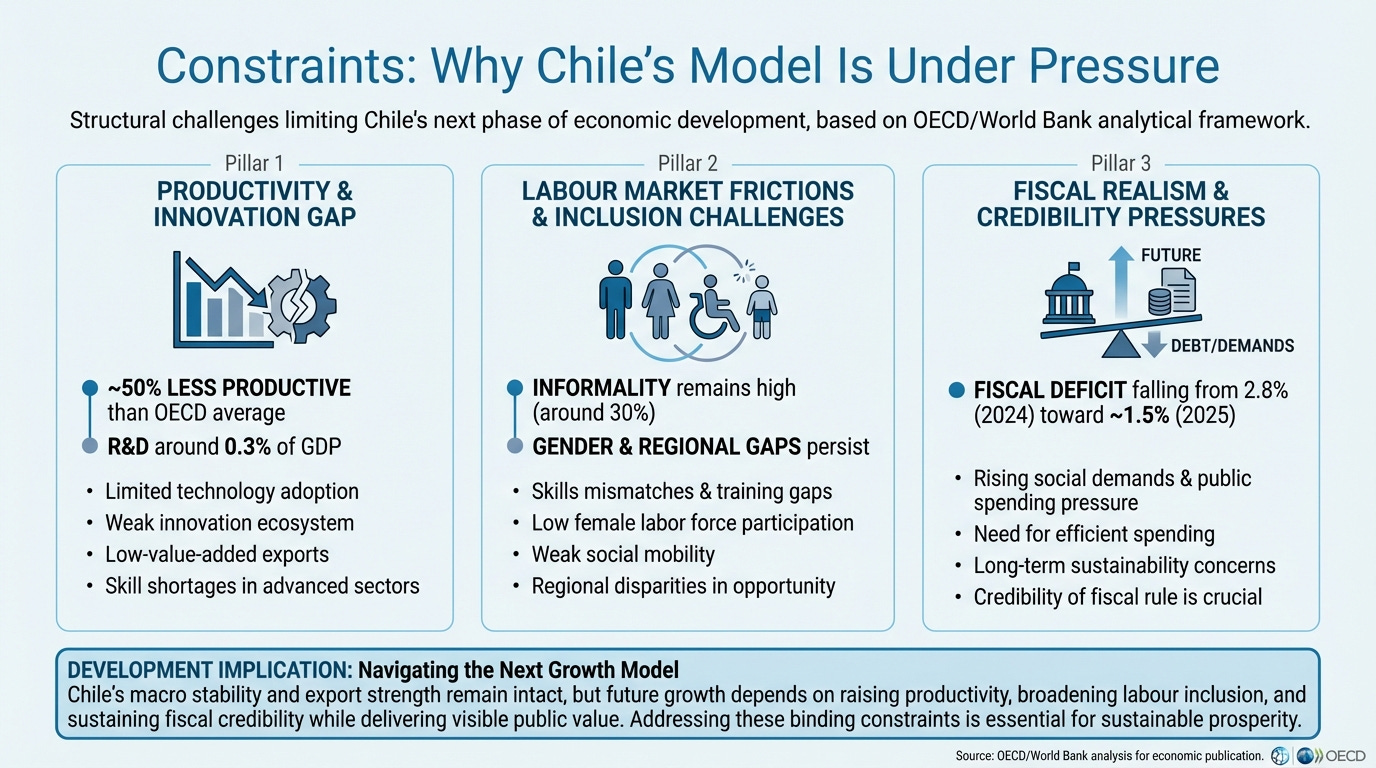

A) Productivity and innovation gap

OECD analysis highlights that Chile’s economy is about 50% less productive than the OECD average, and productivity convergence stalled over the last decade. It also notes low R&D intensity (around 0.3% of GDP, far below the OECD average).

For an economy already at high-income status, this is decisive: without productivity growth, wage gains translate into higher unit labour costs and weaker job creation—precisely what Chile’s labour market has recently signalled.

B) Labour market frictions and inclusion

Real wages rose materially over recent years, while productivity remained flat, putting pressure on hiring—especially in labour-intensive sectors.

Inclusion is not only a social objective; it is also a growth strategy. Closing female labour participation and skills gaps is increasingly framed as a route to raising potential growth (more workers, better allocation of talent, more entrepreneurship).

C) Fiscal realism and credibility

Chile’s fiscal institutions remain strong, but consolidation is politically and administratively difficult. The World Bank notes the fiscal deficit fell from 2.8% of GDP in 2024 (with slippage versus targets) and was projected to drop to ~1.5% in 2025, with public debt expected to remain near ~43% of GDP—below a 45% ceiling.

New revenue measures—including reforms such as a Mining Royalty and Tax Compliance law—are expected to support revenues, but their legitimacy depends on transparent allocation and visible public value (regional development, productivity-enhancing infrastructure, and social protection).

5) Development lessons and priorities

Chile’s case is valuable because it shows both what worked—and what must change at high income.

Lesson 1: Rules and credibility are growth assets

Chile’s inflation-targeting regime and structural fiscal approach are not “technical details”; they are institutions that lower risk premia, stabilise expectations and widen policy space in shocks.

Lesson 2: Openness helps—but does not guarantee sophistication

Chile’s trade network is extensive and supports scale in exports and investment flows, but export concentration persists.

The frontier task is to build domestic capabilities that travel across sectors: advanced services, supplier development, digital adoption, and innovation ecosystems.

Lesson 3: The “green transition” is an industrial strategy opportunity

Chile can pair clean power with minerals to compete in low-carbon supply chains. But success depends on the state’s ability to do four things well:

Manage environmental limits (especially water and ecosystem impacts in salt flats).

Secure community consent through credible consultation and benefit-sharing.

Design clear, investable rules that still protect long-term national value.

Invest in enabling infrastructure (transmission, ports, storage) and faster, more coherent permitting.

Lesson 4: Inclusion is macro-critical

High unemployment and informality are not just social issues; they are constraints on demand resilience and political stability. A high-income Chile needs to translate growth into jobs, particularly for women and younger workers, and to align skills with the digital and green transitions.

Conclusion

Chile’s economic development path has entered a new chapter. The old model—macroeconomic stability + trade openness + commodity-led growth—generated major gains and remains a strength. Yet Chile now faces the typical high-income development test: productivity-led growth that is inclusive, innovation-driven, and environmentally sustainable.

The country’s evolving lithium strategy and its rapidly greening electricity system together form a live case study in 21st-century development policy: whether a resource-rich democracy can turn a green transition moment into a diversified, high-productivity economy—while strengthening social legitimacy and managing ecological limits.