Pathways to Economic Diffusion by 2050

High‑Leverage Strategies for Accelerating Economic Development in Emerging Markets

Prosperity diffusion is the process by which productivity, institutional capability, and technology adoption spread from “frontier” economies and hubs to the rest of the world, raising incomes and reducing poverty. The central development question for 2025–2050 is not whether growth is possible—many emerging markets have demonstrated it is—but whether the world can scale the conditions that make growth broad‑based, durable, and resilient enough to deliver a universal reasonable standard of living by mid‑century.

This report frames poverty reduction as structural transformation, not only as GDP growth. The practical objective is to move households above basic‑needs poverty benchmarks and keep them there, through (1) expanding transaction density (more reliable, cheaper exchange across people, firms, and the state), (2) strengthening institutional reliability(credible rules, enforcement, and service delivery), (3) deepening capital formation (mobilising domestic savings, building credit infrastructure, and improving investment allocation), and (4) integrating markets at scale (within countries, across borders, and into global value chains). These four mechanisms reinforce each other: transaction rails make markets work, reliable institutions make rails trusted, capital formation makes growth investable, and integration makes scale economically meaningful.

The highest‑impact “gear ratio” initiatives—those that generate outsized system‑wide gains relative to their cost and complexity—are platform investments. At the top of the list is interoperable Digital Public Infrastructure (DPI): shared digital systems for identity, payments, data exchange, and registries that enable secure interactions between citizens, firms, and government. DPI is increasingly treated by multilaterals as foundational infrastructure—analogous to roads and power grids—because it lowers economy‑wide transaction costs and improves inclusion and service delivery.

1. Defining the goal: a universal reasonable standard of living

A credible 2050 poverty objective needs two properties: it must be measurable and it must reflect that poverty is not one fixed threshold forever. International poverty lines are periodically updated to reflect changes in global prices and evolving standards. For example, the World Bank’s global poverty lines have been updated over time using Purchasing Power Parities (PPPs); recent updates include revisions to the extreme poverty line and to poverty lines more relevant for middle‑income contexts.

For the purposes of prosperity diffusion, a “reasonable standard of living” is best treated as a policy target band rather than a single number: households should reliably meet basic needs (food, clothing, shelter, energy access, connectivity) and have the capability to invest in human capital and withstand shocks. The implication is that success requires both crossing poverty thresholds and reducing vulnerability to falling back under them—especially under climate, health, and macroeconomic shocks.

2. A development economics framework for prosperity diffusion

Traditional growth narratives often emphasise capital accumulation and human capital. Those are necessary but insufficient. Prosperity diffusion depends on whether an economy can consistently convert labour, capital, and knowledge into productive, tradable output, while maintaining social and political legitimacy.

A practical diffusion framework can be summarised as four interacting “engines”:

2.1 Transaction density: making exchange cheap and reliable

Most emerging markets face a “high friction equilibrium” where information is expensive to verify, payments are costly or slow, and contracts are difficult to enforce. High friction limits market size, keeps firms informal and small, and reduces competition. Raising transaction density—more transactions per person and per firm at lower cost—creates the micro‑foundation for productivity growth.

2.2 Institutional reliability: rules that work in practice

Institutional quality is often framed abstractly. For diffusion, the relevant concept is reliability: can firms predict enforcement, can citizens trust systems, can the state deliver benefits and collect revenue without excessive leakage? Reliability is what turns investment from speculative to scalable.

2.3 Capital formation: mobilising and allocating finance

Many emerging markets have capital, but it is often misallocated or trapped in informal assets, precautionary savings, or low‑productivity sectors. Deepening capital formation means improving the financial plumbing—credit infrastructure, collateral frameworks, risk pricing, and investor protection—so savings become investable capital for productivity upgrades.

2.4 Market integration: scale as a productivity accelerator

Fragmentation is a growth tax. Countries (and regions within countries) that cannot achieve scale face higher unit costs, weaker competition, and thinner labour markets. Integration includes trade facilitation, logistics, standards, and cross‑border payment interoperability.

3. The gear ratio principle: why platforms dominate projects

A “gear ratio” initiative has three features:

Cross‑sectoral spillovers: it improves performance in many sectors at once.

Complementarity: it raises the returns on other investments (it’s a multiplier, not just an additive benefit).

Scalability: it can expand from pilots to national or regional scale without prohibitive marginal costs.

By that definition, the most effective pathways to prosperity diffusion are those that improve an economy’s operating system—especially transaction rails, power reliability, and market integration—rather than narrow programmes that help only one segment.

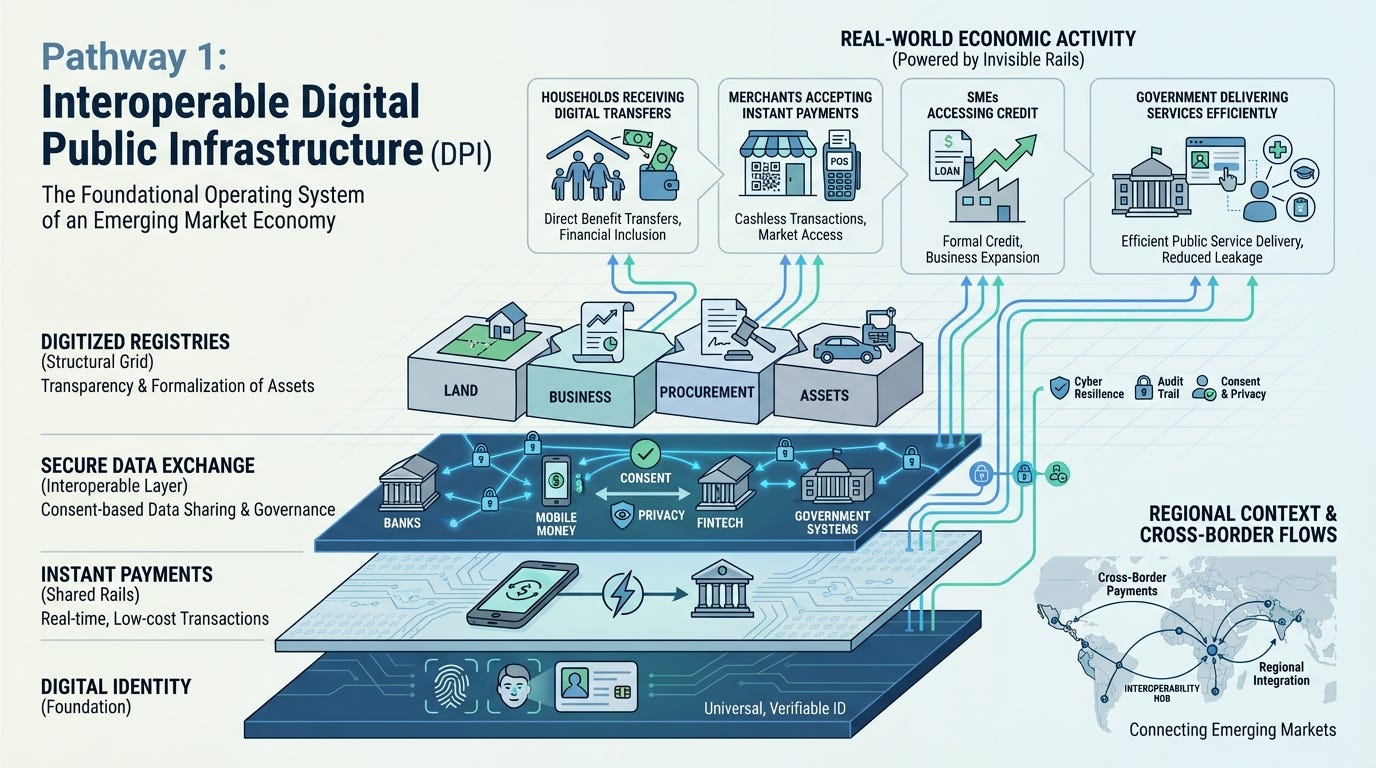

4. Pathway 1: Interoperable Digital Public Infrastructure (DPI)

4.1 What DPI is and why it matters

DPI is widely defined as a set of foundational digital systems enabling secure, seamless interactions among people, businesses, and governments, including identity verification, fast payments, and safe data exchange. The World Bank similarly frames DPI as including digital forms of identification and verification, payments, data exchange, and information systems that underpin service delivery and inclusion.

DPI accelerates prosperity diffusion through multiple channels:

Lower transaction costs: cheaper verification and payments expand market participation.

Formalisation with less coercion: digital receipts, e‑invoicing, and simplified regimes reduce the “paper tax” that pushes firms informal.

Financial deepening: transaction data improves risk assessment for credit, insurance, and merchant services.

State capacity: digitised government‑to‑person (G2P) payments and data sharing reduce leakage and improve targeting.

Innovation ecosystems: open, interoperable rails allow private firms to compete on services rather than rebuilding infrastructure repeatedly.

4.2 Payments as the adoption wedge

In many contexts, fast payments provide the quickest pathway to mass adoption because they are immediately useful to households and merchants. BIS work describes fast payment systems as enabling swift retail payments with rapid funds availability and broad service availability for end users. The World Bank’s FASTT programme also emphasises immediate funds availability and 24/7/365 usability as defining characteristics of retail fast payments.

Latin America illustrates how a payments rail can become ubiquitous. Brazil’s central bank describes Pix as an instant payment scheme enabling transfers in seconds at any time, including non‑business days, used by people, firms, and government. This type of adoption compresses the distance between informal and formal commerce: when small merchants can accept digital payments cheaply, the economy produces more verifiable transaction history—fuel for broader financial services.

4.3 Africa’s advantage and constraint: mobile-first scale, fragmented interoperability

Sub‑Saharan Africa demonstrates that transaction rails can scale even where traditional banking penetration is limited, through mobile money and agent networks. GSMA reporting shows the immense scale of mobile money globally and highlights Sub‑Saharan Africa as a leading region, with large numbers of registered accounts and high transaction volumes. The frontier now is less “can digital transactions work?” and more “can markets interoperate across providers and borders?” Interoperability is the step that turns national success stories into regional prosperity diffusion.

4.4 The trust layer: privacy, cyber risk, and governance

DPI is powerful precisely because it concentrates systemic capability—so failures can be systemic too. Large‑scale payment ecosystems create new attack surfaces, and cyber incidents can carry macro‑level consequences. Reporting on cyberattacks targeting widely used payment infrastructure underscores that scaling digital rails must be matched with operational resilience, credential security, and rapid incident response.

For DPI to accelerate inclusion rather than undermine legitimacy, safeguards must be built in: data minimisation, consent and auditability, grievance redress, competitive neutrality, and independent oversight. These are not “nice to have”; they are adoption conditions.

5. Pathway 2: Power reliability reform as a productivity multiplier

Electricity is not merely “infrastructure”; it is the operating constraint behind manufacturing competitiveness, cold chain viability, service sector productivity, and the digital economy itself. The most important distinction for 2025–2050 is between adding generation capacity and delivering reliability. Many emerging markets have enough installed capacity on paper but fail on distribution losses, maintenance, billing/collection, and governance.

Power reliability reform is high gear ratio because it multiplies the returns on nearly every other intervention: DPI needs connectivity and stable power; industrial clusters need predictable electricity; urbanisation becomes productive when services are reliable. The development playbook here is practical and unglamorous: reduce technical and commercial losses, improve metering and collections, align tariffs with cost recovery while protecting the poor through targeted subsidies, and build credible utility governance that can maintain assets over decades.

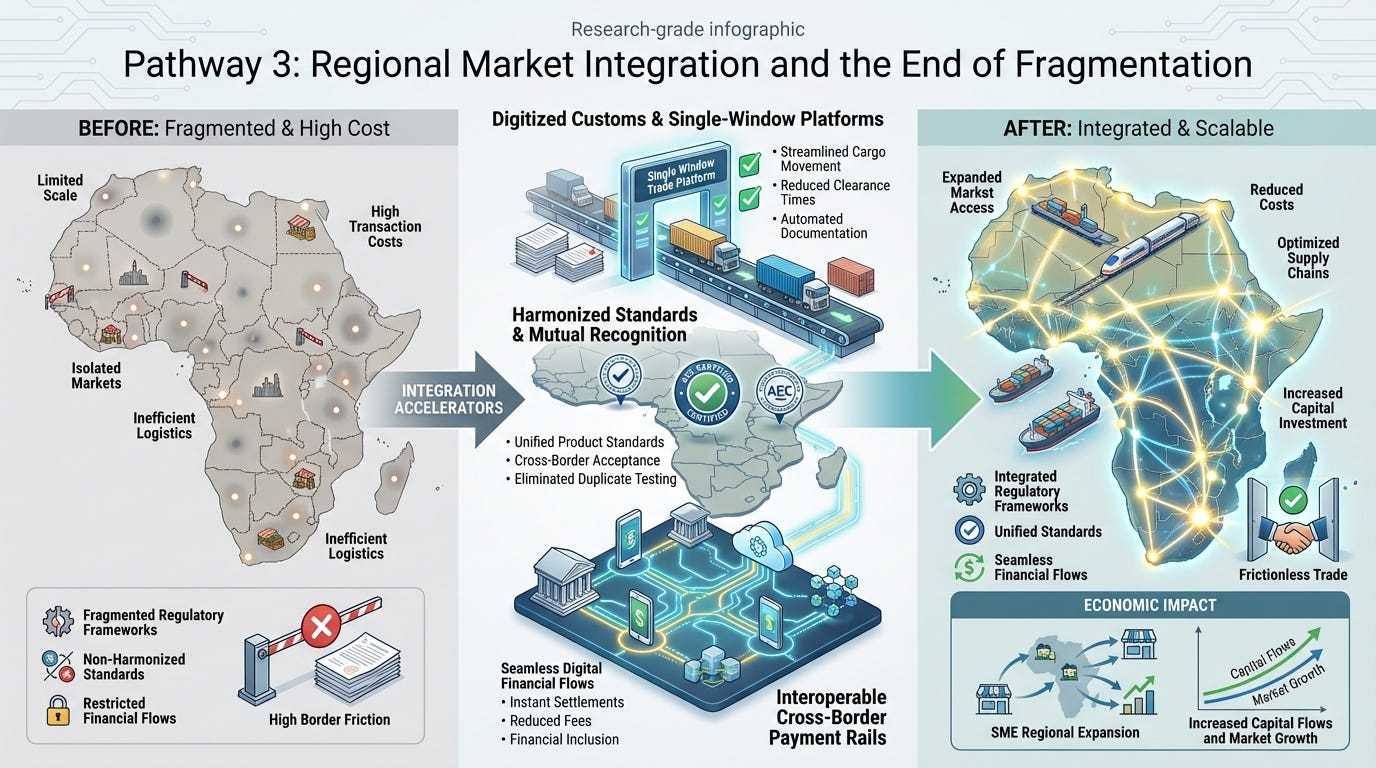

6. Pathway 3: Regional market integration and the end of fragmentation

Fragmentation is a silent poverty trap. Small, segmented markets reduce competition, lower firm scale, and increase the cost of logistics and compliance. Regional integration is therefore not an “optional” trade agenda—it is a structural transformation agenda.

The most powerful integration accelerators for 2025–2050 are:

Trade facilitation: single‑window customs, risk‑based inspections, and digitised documentation that reduces border delays.

Standards and mutual recognition: making it cheaper for firms to sell across borders.

Cross‑border payment interoperability: reducing the cost of remittances and trade payments and enabling regional e‑commerce.

When combined with DPI, regional integration becomes a compounding platform: firms can scale across borders using common rails; workers and entrepreneurs can participate in larger markets; and investment becomes more attractive as market size increases.

7. Pathway 4: Urban land formalisation and investable cities

Prosperity diffusion largely happens through cities because cities concentrate labour markets, infrastructure, services, and demand. But urbanisation alone does not produce prosperity; productive urbanisation does. The difference is whether cities can mobilise capital and deliver services at scale.

Urban land and property formalisation—digitising cadastres, clarifying tenure, enabling transparent transfers, and creating predictable permitting—has a large gear ratio because it unlocks three things at once:

Collateral and credit: property becomes investable and financeable.

Municipal revenue: cities can fund services and infrastructure credibly.

Private sector building: housing supply and commercial development can scale.

Without functioning land markets, urban growth tends toward informality, congestion, and high living costs—conditions that blunt the demographic dividend.

8. Pathway 5: SME credit infrastructure and productive formalisation

SMEs are the employment engine in most emerging markets, but they are frequently stuck in low‑productivity equilibria due to lack of finance, unreliable demand, and high compliance burdens. The prosperity diffusion objective is not to make every microenterprise formal overnight; it is to enable a pipeline where high‑potential firms can graduate: from informal to semi‑formal to fully formal, accessing credit, technology, and new markets.

High‑leverage components include:

Credit infrastructure: credit bureaus, secured transactions frameworks, collateral registries, and predictable enforcement.

Open finance and data portability: enabling competition in credit and merchant services, provided privacy safeguards are credible.

Digitised compliance: e‑invoicing and simplified tax regimes that lower administrative burdens while widening the base.

In practice, SME credit deepening works best when built on top of transaction rails: payments data becomes an input to credit scoring; e‑invoicing becomes an input to working capital; procurement platforms become a pathway to stable demand.

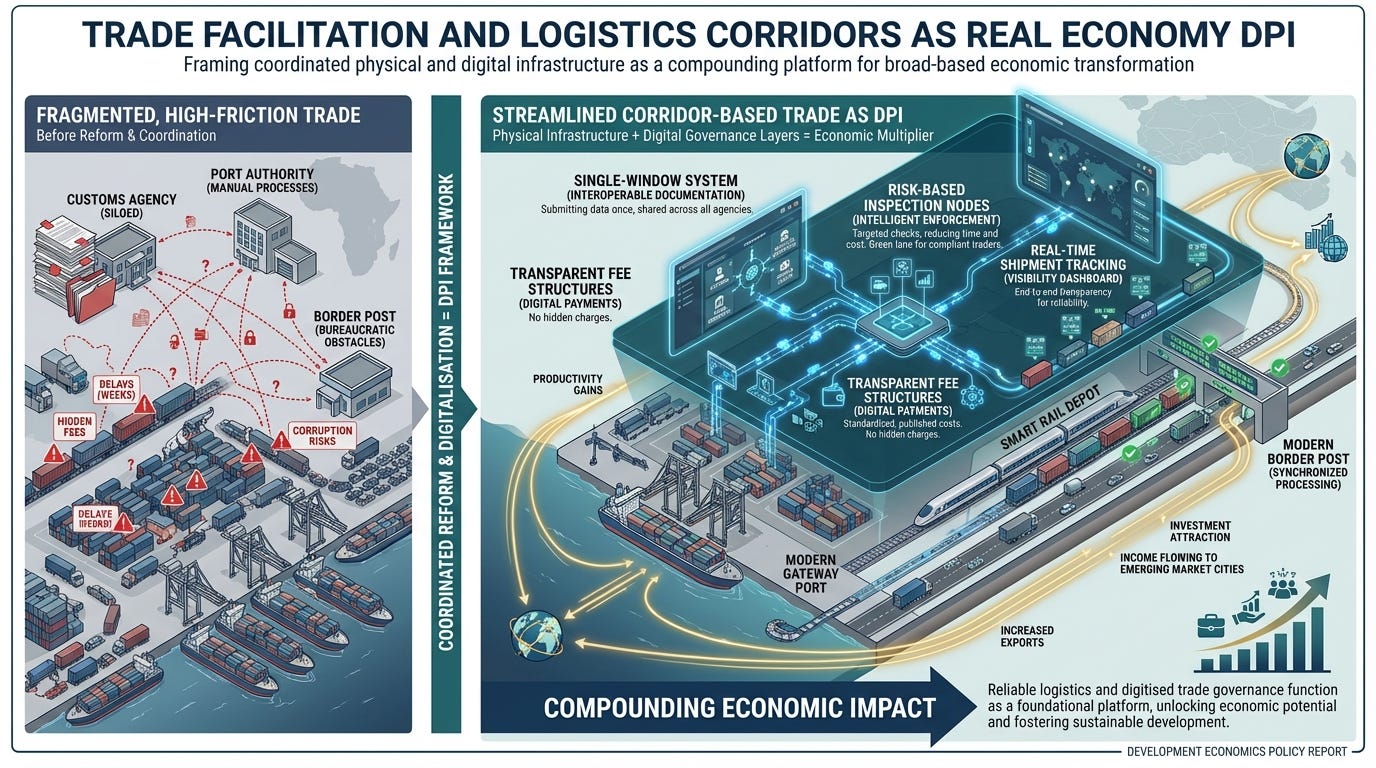

9. Pathway 6: Trade facilitation and logistics corridors as “real economy DPI”

Trade is where productivity becomes income at scale. For many emerging markets, especially in Africa and parts of Latin America, the binding constraint is not the ability to produce something; it is the cost and reliability of getting it to market. Targeted corridor and port reforms can be high gear ratio when they reduce time and uncertainty for the entire tradable sector.

Digitisation matters here as much as concrete: single‑window systems, transparent fee structures, tracking systems, and risk‑based inspections often deliver outsized gains relative to heavy infrastructure, especially in the first decade (2025–2035). Physical upgrades then become more valuable once governance and throughput reliability improve.

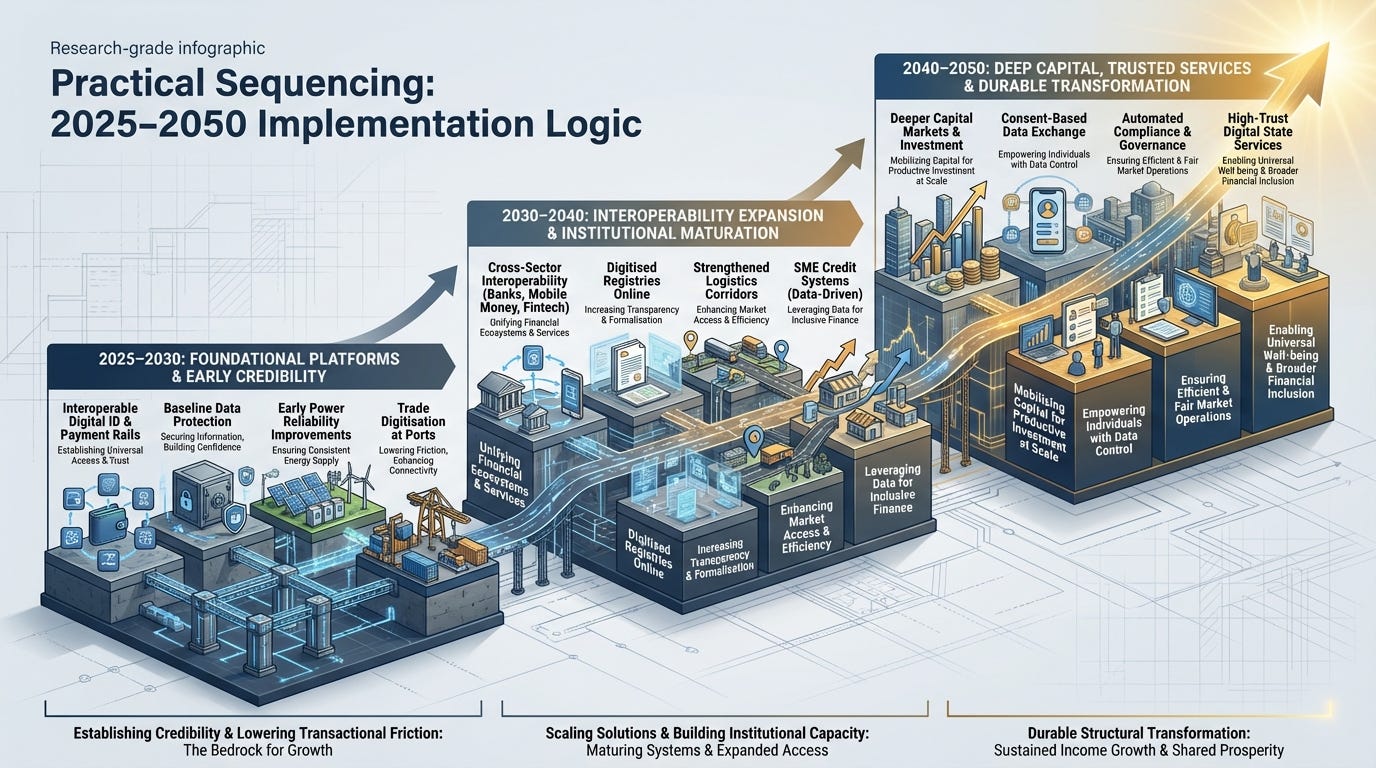

10. Practical sequencing: 2025–2050 implementation logic

The core implementation insight is that prosperity diffusion is path dependent. Early wins build adoption, legitimacy, and fiscal space; later reforms deepen the economy’s complexity.

2025–2030: Build minimum viable national platforms

The priority is to establish the foundations that make everything else easier:

DPI adoption wedge: fast payments + merchant acceptance + anchor government use cases (payroll and G2P)

Identity expansion with strong inclusion and grievance redress

Baseline data protection and operational cybersecurity capacity

Power reliability pilots in priority metros and industrial zones

Trade facilitation digitisation at major ports and borders

This is the “lower friction now” decade: remove the most expensive sources of delay, leakage, and exclusion.

2030–2040: Interoperate, formalise, and scale productive investment

Once rails exist, the goal becomes market expansion and capital deepening:

Interoperability across banks, mobile money, and fintech on common rails

Digitisation of land and business registries (starting urban/peri‑urban)

E‑procurement and public finance transparency

Logistics corridors and standards infrastructure

SME working capital systems driven by invoicing and transaction histories

This is the decade where informality can shrink meaningfully without coercion, because markets become more investable and compliance becomes less punitive.

2040–2050: Deepen verification and unlock broader capital markets

The final decade focuses on maturity:

Consent‑based verification and data exchange layers for lower fraud and lower onboarding cost

Automated compliance for SMEs and supply chains

Stronger collateral frameworks and local currency finance

High‑trust digital state services that reduce the administrative burden (“paper tax”) economy‑wide

The prize here is durability: an economy that is not only richer, but more resilient and governable.

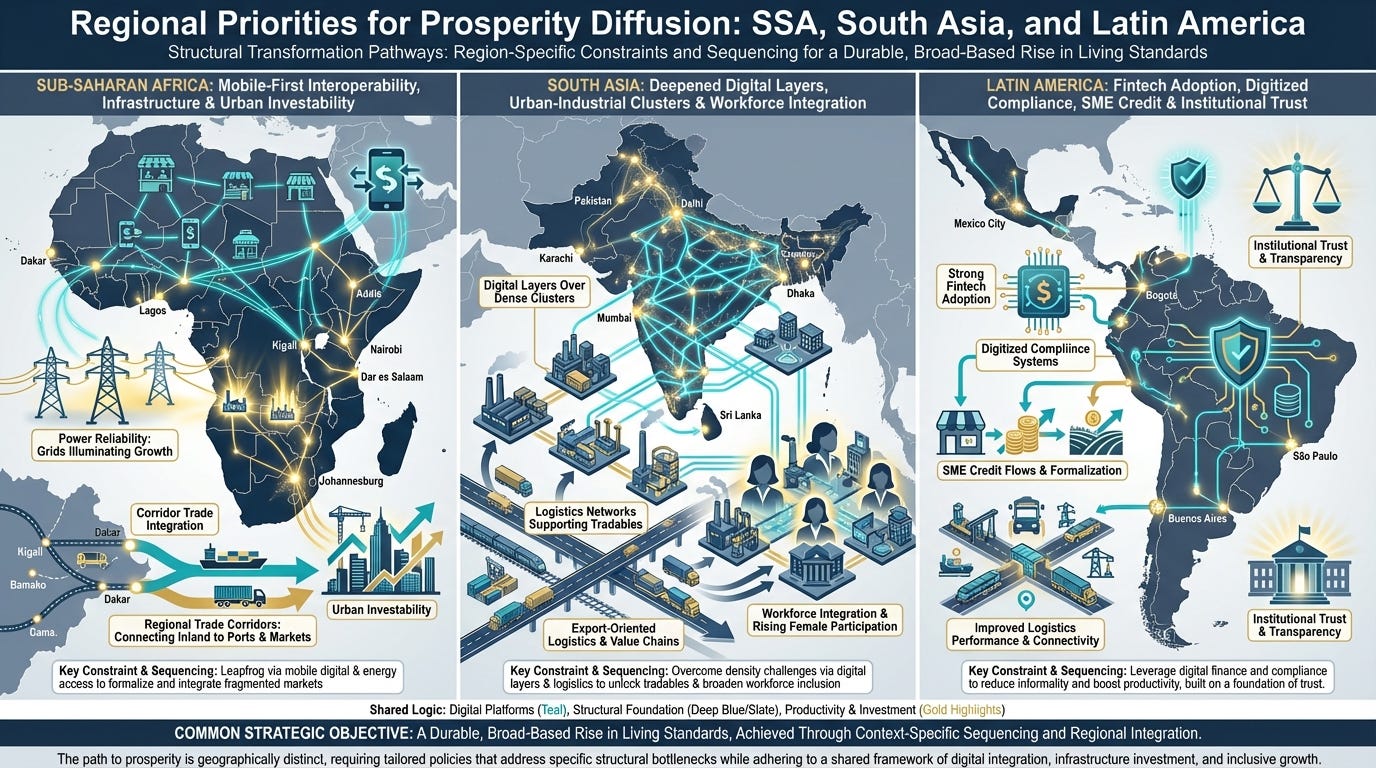

11. Regional emphasis: how priorities differ across SSA, South Asia, and Latin America

Sub‑Saharan Africa: interoperability, power reliability, and urban investability

Africa’s opportunity is demographic and entrepreneurial; its constraint is fragmentation and infrastructure reliability. The highest gear ratio agenda typically combines (1) mobile‑first DPI interoperability across providers, (2) power reliability in priority cities and industrial clusters, (3) corridor trade facilitation for regional scale, and (4) urban land reforms to make cities investable. GSMA’s evidence of mobile money scale suggests a strong base on which to build interoperability and broader financial services.

South Asia: deepen platforms, expand female labour participation, and scale tradables

South Asia’s differentiator is its large workforce and dense markets. The diffusion agenda tends to be about (1) deepening DPI and data exchange, (2) logistics and industrial cluster competitiveness, (3) skills linked to tradable sectors, and (4) policies that raise labour participation and mobility. The sequencing still starts with platforms, but the binding constraints are often jobs and productivity absorption rather than basic adoption.

Latin America: productivity, security of transactions, and formalisation with trust

Latin America’s challenge is frequently not adoption of digital services—many countries have strong fintech ecosystems—but raising productivity and formalisation while maintaining social legitimacy. Payments infrastructure like Pix illustrates what rapid adoption can look like when rails are simple and ubiquitous. The highest gear ratio agenda often focuses on (1) lowering compliance burdens through digitisation, (2) improving logistics and trade performance, (3) unlocking SME credit at scale, and (4) strengthening state effectiveness to reduce leakage and improve trust.

12. Measurement: what to track if the objective is diffusion, not anecdotes

A prosperity diffusion scorecard should track leading indicators tied to the four engines:

Transaction density: share of adults and SMEs using digital payments; merchant acceptance density; cost and speed of transfers; share of government payments digitised.

Institutional reliability: service delivery performance, procurement transparency, grievance resolution rates, and audit outcomes.

Capital formation: SME credit penetration, collateral registry usage, domestic savings mobilisation, and local currency finance depth.

Market integration: border clearance times, logistics performance, cross‑border payment costs, and standards recognition.

These indicators predict whether poverty reduction will be fast and durable, rather than temporary.

13. Risks and failure modes: why high‑leverage can also be high‑stakes

High gear ratio initiatives concentrate power and capability; the downside risks are therefore systemic:

Surveillance and exclusion: if DPI is used as a control tool or excludes marginalised groups, adoption collapses and legitimacy erodes.

Cybersecurity and operational concentration: widely used payment systems and data platforms can become targets; resilience and credential security must scale with adoption.

Monopoly capture and vendor lock‑in: closed systems reduce competition and raise costs long‑term, limiting diffusion.

Implementation without institutions: infrastructure deployed without credible governance underperforms or is captured.

The remedy is not to slow down platforms; it is to build trust architecture (privacy, competition, oversight) in parallel.

Conclusion: the most effective pathways are “operating system upgrades”

If prosperity diffusion is the objective, the 2025–2050 agenda is not primarily a search for one breakthrough sector; it is the deliberate scaling of platforms that reduce friction, improve reliability, and enable markets to integrate and invest. Interoperable DPI, fast payments, and secure data exchange are central because they lower transaction costs across the whole economy and enable both private innovation and state capacity. Power reliability reform multiplies every other investment. Regional integration turns fragmented economies into scalable markets. Urban land formalisation turns cities into investable engines of productivity. SME credit infrastructure turns entrepreneurship into growth at scale. Trade facilitation converts productivity into income through tradables.

By mid‑century, a world in which most people enjoy a reasonable standard of living is plausible if these high‑leverage platforms are implemented with strong governance and sequenced for compounding effects. The decisive question is not whether these tools exist—they do—but whether institutions and coalitions can deploy them fast enough, fairly enough, and credibly enough to make prosperity diffuse before demographic and climate pressures overwhelm the opportunity.