Transaction Infrastructure as a Development Engine

Why “identity + payments + data exchange + registries” is the highest‑leverage investment for prosperity diffusion (with lessons from Africa, India, and Latin America)

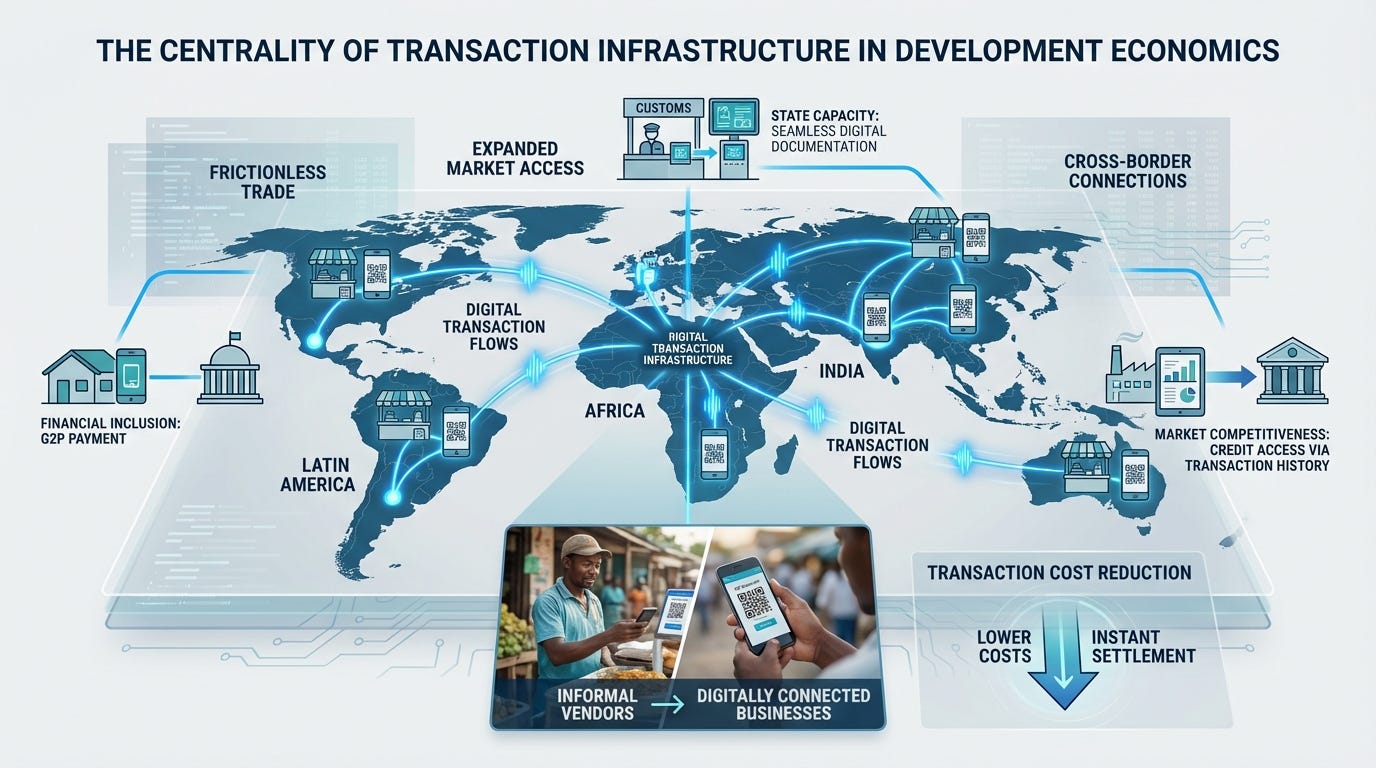

“Transaction infrastructure” is the foundational set of digital rails and institutional rulebooks that make everyday economic activity cheap, trustworthy, and scalable: who you are (identity), how you pay (payments), how verified information moves (data exchange), and what is recorded (registries such as land, firms, and civil status). When these rails work well, they compress transaction costs across the whole economy—expanding market access, enabling formalisation, improving state capacity, and making social programmes more effective and less leaky. The World Bank increasingly frames these shared rails as Digital Public Infrastructure (DPI)—core systems such as digital ID, payments, and data-sharing that governments and firms can build upon to deliver services and enable inclusive growth.

From a development economics perspective, transaction infrastructure is powerful because it changes the “friction level” of an economy. It raises productivity not by targeting one sector, but by improving the coordination and trust conditions under which all sectors operate. It also shifts poverty reduction from being limited by administrative capacity (who is eligible? how do we pay?) to being limited by policy choices and financing—which is a much better problem to have.

1. What “transaction infrastructure” actually means

In practical terms, transaction infrastructure is the stack that allows people, firms, and the state to transact reliably at scale:

The core rails

Digital identity and authentication

A way to uniquely and securely verify a person (or business) so they can open accounts, access services, and receive benefits.Interoperable instant/fast payments

A payment system that moves money quickly with immediate availability of funds for recipients, supporting retail payments at scale. Fast payment systems are now widely deployed globally and are a key design pattern for modern retail payments.Secure data exchange / consent-based verification

A mechanism for organisations to verify claims (income, residency, licences, education credentials) without repeatedly collecting paper documents—reducing fraud and administrative burden. Estonia’s X‑Road is a well-known example of a national interoperability/data exchange layer.Authoritative registries

Digitised registries for land and property, business incorporation, civil registration, licences, and often procurement and public finance—the “ledgers” that make rights enforceable and markets investable.

The enabling rulebook

Data protection and cybersecurity

Competition and interoperability standards

Dispute resolution and consumer protection

Governance and oversight (audits, grievance redress, accountability)

Without the rulebook, the rails either fail (low trust) or become extractive (high surveillance, monopoly rents, elite capture).

2. Why transaction infrastructure is so central in development economics

Development is not only about adding capital and labour; it is about improving coordination: reducing the costs of finding counterparties, verifying information, enforcing agreements, and moving value.

Transaction infrastructure is a direct assault on those coordination costs.

A. Lower transaction costs → bigger and more competitive markets

When payments are instant and cheap, and identity/KYC is simpler, small firms can sell beyond local geographies, customers can pay digitally, and suppliers can be onboarded quickly. This expands market size and increases competition—two of the most reliable drivers of productivity growth.

Fast payment systems are explicitly designed to make retail transactions swift with immediate availability of funds, which can materially change how households and businesses transact.

B. Financial inclusion that goes beyond “accounts”

In many low- and middle-income countries, the constraint is not whether people want financial services—it’s whether providers can serve them profitably and safely. When identity and payments rails are ubiquitous, the private sector can layer on savings, credit, insurance, and merchant services.

In Sub-Saharan Africa, mobile money has become a dominant channel for everyday payments, demonstrating how transaction rails can scale even where legacy banking is thin.

C. Formalisation without heavy bureaucracy

A high-friction state often “taxes” firms in time, bribes, and delays—pushing activity into informality. Transaction infrastructure enables “soft formalisation”:

e-registration of firms

e-invoicing / digital receipts

simplified digital tax regimes

traceable payments

That can widen the tax base and improve compliance without relying on coercive enforcement.

D. State capacity and service delivery (especially G2P)

The state is one of the biggest “platform customers” of transaction infrastructure. Once people can be identified and paid digitally, governments can deliver benefits with far less leakage, and can run policy with more precision. The World Bank explicitly links DPI to inclusion, resilience, and improved delivery—particularly through digital ID and digitised government-to-person payments.

3. The Transaction Infrastructure Stack

A useful way to frame it is as a layered stack:

Layer 1 — Identity

Purpose: establish unique, verifiable participation in the economy

Development payoff: inclusion, formalisation, targeted transfers, trust in services

India’s Aadhaar is positioned by UIDAI as foundational identity and authentication infrastructure supporting access to entitlements and digital services.

Layer 2 — Payments

Purpose: move money instantly and cheaply between people, firms, and government

Development payoff: merchant growth, SME liquidity, e-commerce, reduced cash frictions

Brazil’s central bank describes Pix as an instant payment scheme enabling transfers within seconds, available any time including non-business days.

Layer 3 — Data exchange and verification

Purpose: verify claims (who, what, where) without paper-chasing

Development payoff: lower fraud, faster onboarding, less bureaucratic drag

X‑Road is described as a secure data exchange layer connecting databases across public and private sectors.

Layer 4 — Registries and workflow systems

Purpose: digitise rights and obligations (land, firms, licences, procurement)

Development payoff: investment, collateral, enforceability, transparency

Layer 5 — Governance, safeguards, and accountability

Purpose: maintain trust and prevent capture/misuse

Development payoff: adoption, durability, and political legitimacy

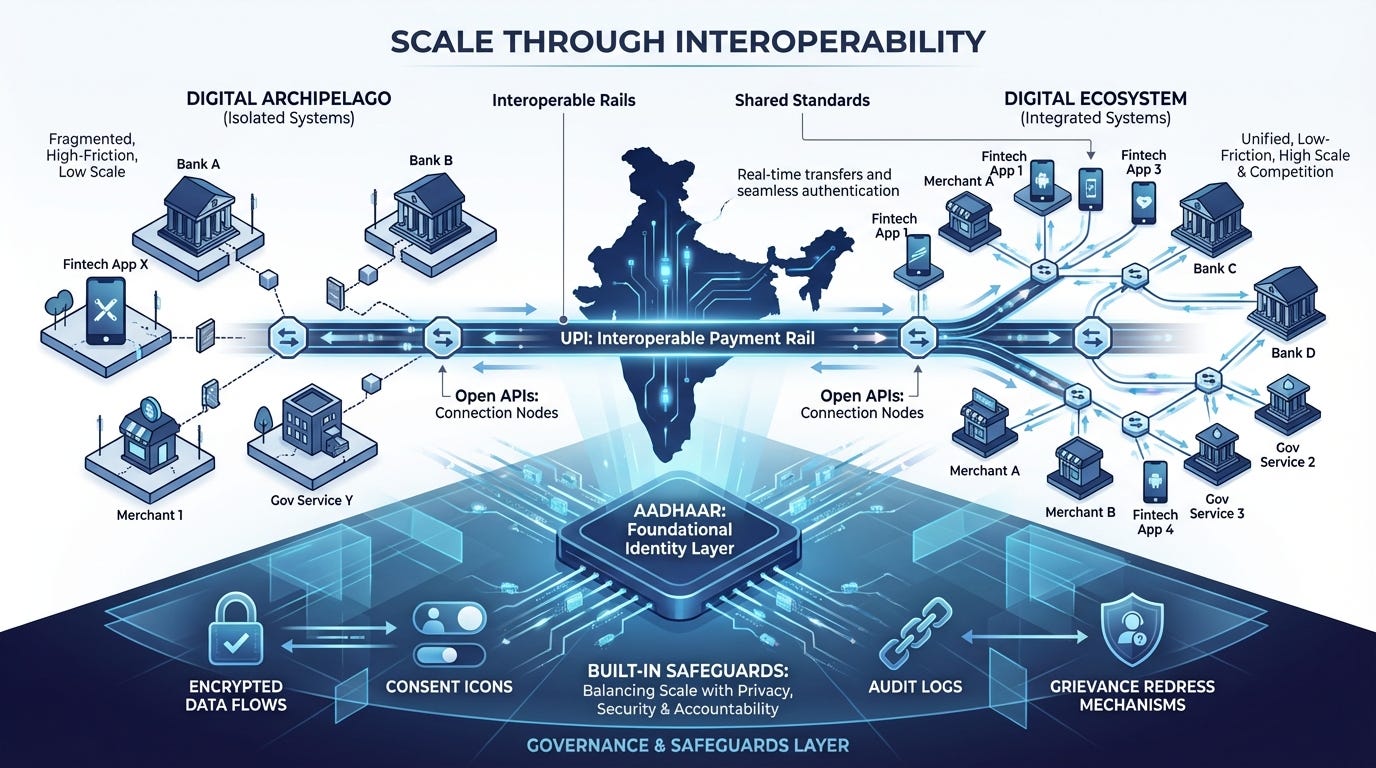

4. Lessons from India: scale through interoperability

India’s tale is often summarised as “identity + interoperable payments + open APIs”.

UPI is widely recognised as a major innovation in retail digital payments launched by NPCI and enabling easy, real-time transfers and merchant payments.

Aadhaar is positioned as an enabling identity/authentication layer that supports access to services and benefits.

The development lesson

Interoperability is the difference between a digital ecosystem and a digital archipelago. When many banks and apps can plug into one set of rails (with common standards), innovation shifts from building closed-loop systems to building services on top of shared infrastructure.

The caution

At population scale, the risks—privacy, surveillance, exclusion errors, cyber threats—also scale. The design must include safeguards (data minimisation, consent, auditability, grievance redress) from day one, not as an afterthought.

5. Lessons from Latin America: Pix and the “payments-first” pathway

Latin America is instructive because it includes both high informality and strong fintech dynamism.

Brazil’s Pix demonstrates a central bank-led approach to instant payments at national scale: the central bank’s own description emphasises real-time transfers in seconds, available at any time, used by people, companies, and government.

The development lesson

“Payments-first” can be a credible strategy where:

mobile penetration is high,

cash is costly, and

informal commerce dominates.

Payments rails quickly create merchant adoption, transaction records, and a platform for credit scoring—then identity, registries, and data exchange deepen the system.

The caution

Instant payments can also accelerate fraud if consumer protection and dispute mechanisms lag. The “rulebook layer” must mature alongside the rails.

6. Lessons from Africa: mobile-first rails, but interoperability is the frontier

Sub-Saharan Africa has the world’s most distinctive transaction infrastructure reality: mobile money is not a fintech edge-case; it is mainstream financial plumbing.

GSMA’s reporting highlights the enormous global footprint and growth of mobile money, with Sub-Saharan Africa as a leading region.

Safaricom describes M‑PESA as a service enabling transfers and payments—illustrating the practical, consumer-facing shape of this infrastructure.

The development lesson

Africa shows that transaction infrastructure can scale even with:

limited bank branch density,

high informality,

weak legacy registries, and

constrained state capacity.

Agent networks, USSD/offline workflows, and mobile-first product design can substitute for “traditional” infrastructure in the early phases.

The frontier problems (where the next gains are)

Interoperability across networks and borders

Fragmentation raises costs and limits market scale. Regional payment integration and common standards are the next big multiplier.Productive use of rails (beyond P2P transfers)

The growth payoff comes when rails support:

merchant acquiring at scale

SME working capital

procurement and invoicing

logistics and trade payments

Digitising land and business registries

Without registries, firms can’t collateralise, cities can’t plan, and investment remains high-risk.

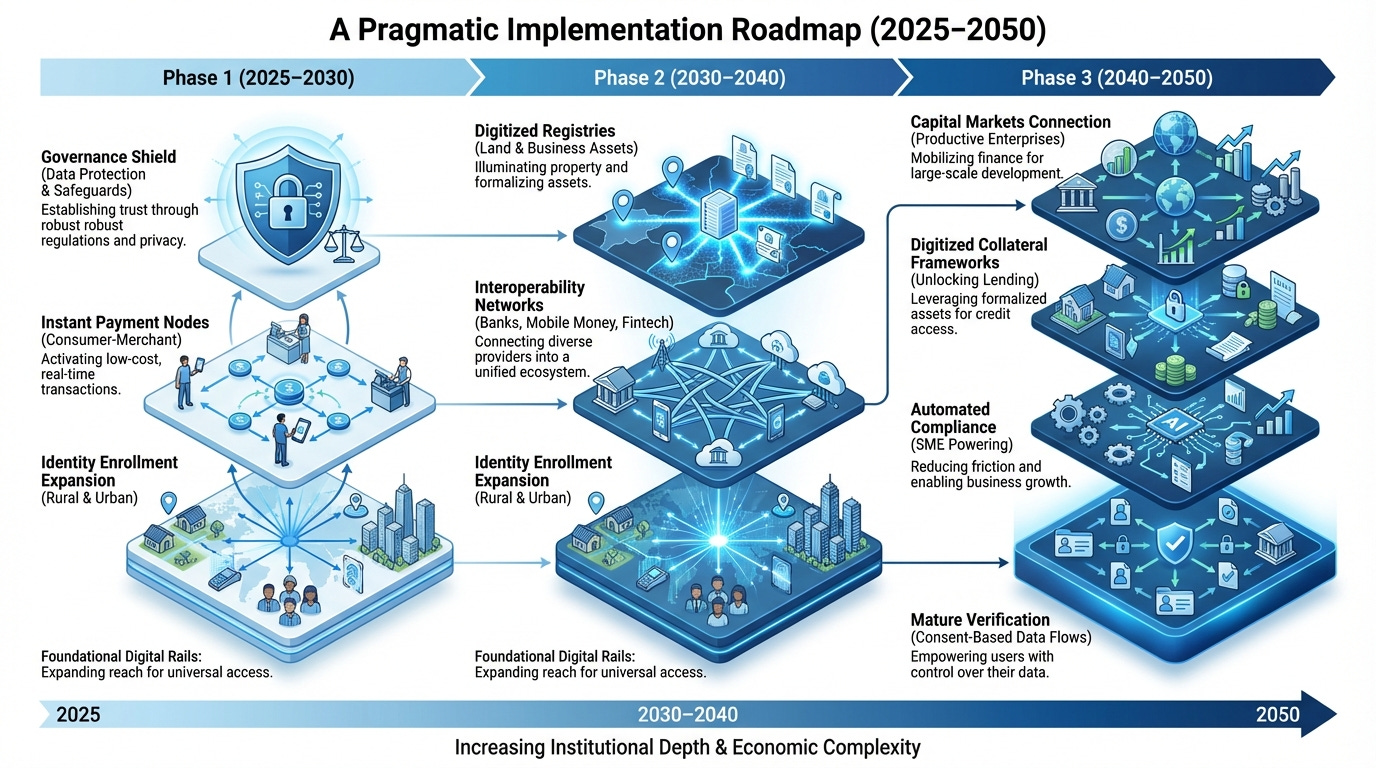

7. A pragmatic implementation roadmap (2025–2050)

A credible transaction infrastructure strategy is iterative and modular.

Phase 1: 2025–2030 — Build minimum viable rails

Identity: expand coverage; prioritise inclusion and grievance redress

Payments: implement or modernise fast payments; enable merchant acceptance

Foundational governance: data protection basics, consumer protection, cyber standards

Government “anchor use-cases”: payroll and G2P transfers (quick wins for adoption)

Phase 2: 2030–2040 — Interoperate and formalise

National interoperability: banks + mobile money + fintech on common rails

Digitise core registries: business, land (starting with urban/peri-urban)

e-Procurement and digital public finance for transparency

Start cross-border corridors for remittances and trade payments

Phase 3: 2040–2050 — Deepen verification and unlock capital markets

Mature data exchange layer (consent-based verification)

Automated compliance for SMEs (e-invoicing, smart tax)

Digitised collateral systems and secured transactions frameworks

High-trust digital state services, reducing the “paper tax” across the economy

8. Design principles that separate success from failure

These are the principles repeatedly associated with durable, scalable transaction infrastructure:

Interoperability by default (avoid walled gardens)

Modular architecture (build once, reuse across sectors)

Inclusion-first (offline options, accessible onboarding, low-cost devices)

Privacy and trust systems embedded (not bolted on later)

Open standards and vendor lock-in resistance

Clear accountability (audits, logs, independent oversight, grievance redress)

Estonia’s X‑Road framing is explicitly about interoperability across many systems while maintaining secure exchange—useful as a “north star” for verification layers.

9. How to measure progress (a practical scorecard)

If you want transaction infrastructure to be more than rhetoric, track metrics that map to real economic frictions:

Coverage and access

% adults with usable identity credentials

% adults and SMEs with access to digital payments

rural/urban and gender gaps

Performance and cost

median time-to-settlement for retail payments

merchant acceptance density

cost to onboard a customer (KYC + account)

uptime and resilience

Interoperability and competition

number of interoperable participants (banks, wallets, fintechs)

cross-network payment completion rate

concentration metrics (market power / monopoly risk)

Governance and trust

fraud rates and resolution times

number of complaints resolved via grievance channels

audit findings and procurement transparency

Economic outcomes (lagging but decisive)

SME formalisation rates

credit penetration for small firms

tax base broadening without punitive enforcement

leakage reduction in social transfers

10. Why this matters for “prosperity diffusion” models

In diffusion terms, transaction infrastructure increases the “conductivity” of an economy:

It amplifies the returns to digital connectivity (people can actually transact online).

It raises institutional capacity (the state can implement programmes reliably).

It increases trade openness in practice (faster customs and payments, better compliance, lower friction).

It supports structural transformation (firms can scale, cities become investable, labour becomes more mobile and bankable).

If you’re modelling development as network diffusion, transaction infrastructure is the edge-weight enhancer: it strengthens the links through which productivity and opportunity spread.

Closing view

If you had to prioritise one development investment category that reliably compounds across sectors, transaction infrastructure is near the top. It is not “tech for tech’s sake”; it is the modern equivalent of building roads, property rights, and reliable courts—but optimised for a 21st-century economy where value, identity, and verification increasingly move digitally.